In the last 15 years, “all-in-one apps” that combine dozens of different features have taken the world by storm. This trend began in Asia, where super apps have become the norm, but faces resistance from companies and officials in the West. In his column for TAdviser in February 2024, expert Alexey Titov explains what super apps are and how they’re evolving.

What Is a Super App?

When people talk about a “super app,” they typically refer to services in China where you can do everything from booking a taxi to paying for purchases, showing your airplane ticket, or even buying heavy industrial equipment. Chinese super apps have become so integrated into society that it’s nearly impossible to live without them.

Interestingly, the term was coined 15 years ago by BlackBerry’s founder Mike Lazaridis. He believed that people didn’t need dozens of different apps and that all their functions could be combined into one ecosystem.

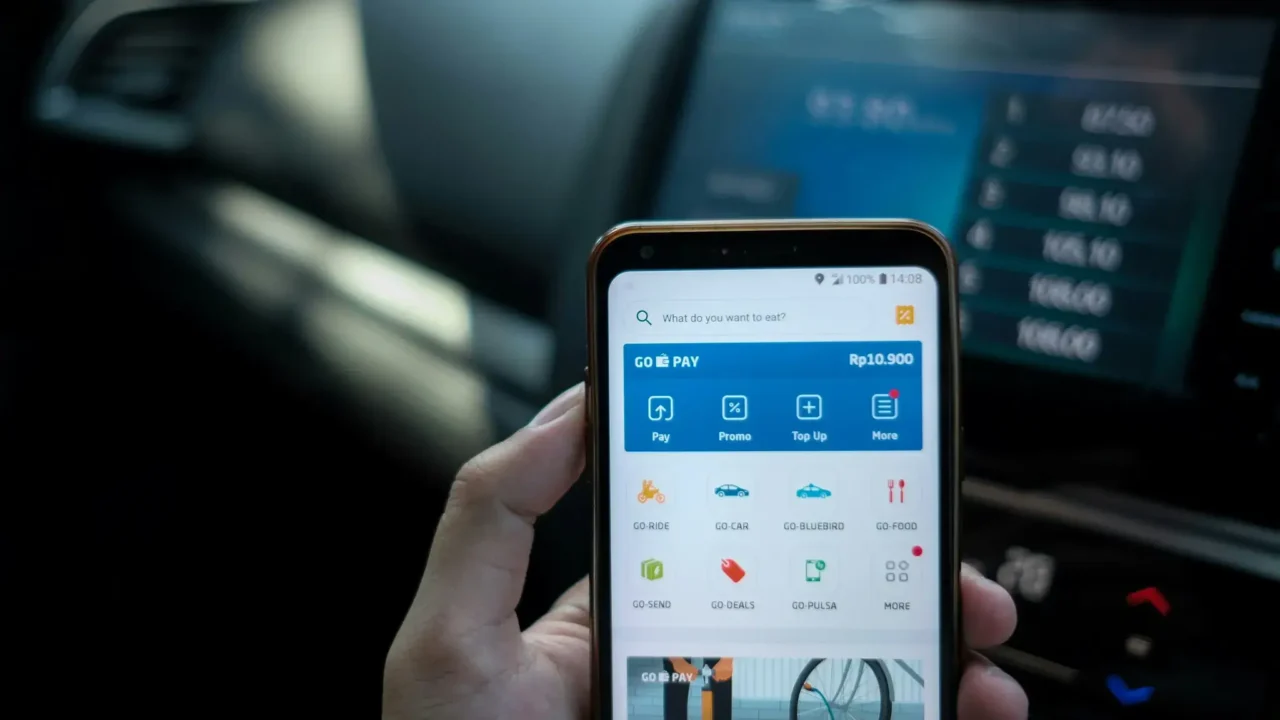

Super apps often start with a single service, such as messaging or taxi booking, then evolve to include other functionalities: food delivery, digital payments, bill payments, mobile phone top-ups, audio and video streaming, social networks, and forums. Super apps can encompass virtually any feature, including cryptocurrency investing and election voting.

Are Super Apps Really That Popular?

Yes, they are. The most popular super app in China (let’s call it “Yellow”) has over 1.2 billion users. Other super apps have emerged in India, Singapore, South Korea, Vietnam, and Indonesia.

In 2024, it’s almost impossible to use a traditional bank card in China—most transactions are handled through super apps. China is the first cashless country in the world.

The total number of super app users exceeds 2.5 billion. You likely have one or two on your smartphone. A well-known Russian bank is trying to develop its app into a super app, and a major Russian IT company has been releasing super apps for over a decade.

Why Are They So Popular in Asia?

Their popularity is primarily due to the “Great Mobile Shift.” A whole generation in China, India, and Southeast Asian countries grew up with smartphones as their first devices. Over 80% of smartphone owners in Asia don’t own desktop computers or laptops, making traditional website or service access difficult for them.

The “Great Mobile Shift” led to phenomena that were unimaginable a decade ago. According to KPMG, 73% of people in South and Southeast Asia don’t have bank accounts—they simply don’t need them. The equivalent of a bank account is a digital wallet within a super app. It’s likely that the ratio of people without bank accounts is even higher in Africa.

China lacks capital regulation rules for super app users’ funds, allowing super apps to invest in overnight funds, place money in interest-bearing accounts, and engage in unregulated peer-to-peer lending. These services don’t share crucial financial data with regulatory bodies or implement anti-money laundering measures.

Moreover, super apps in China enjoy substantial government support, with officials integrating over 200 government services into these apps. The “Yellow” Chinese super app even replaces a citizen’s ID card.

Why Are Super Apps Not As Popular in Western Countries?

In the EU and the US, super apps are relatively unpopular, and there’s little indication of a surge in their adoption. Several factors contribute to this:

- Strong Financial Institutions: In countries where most people use bank apps, super apps lose their appeal due to seamless payment services. The financial market in the US and EU is fiercely competitive, and no one wants to give up their position to integrate with a super app.

- Government Regulation: Unlike in Asia, regulatory requirements in the US and Europe are stricter, inhibiting the emergence of a digital provider like a super app. Moreover, antitrust laws prevent the merger of major tech players, while GDPR complicates the aggregation of personal data in Europe.

- Data Privacy Concerns: People in Western countries are traditionally more concerned about data privacy. In Germany, for example, data protection is so strict that it hampers the state’s ability to collect large-scale citizen data.

- Advertising Revenue: Western companies earn significant revenue from advertising, and merging apps into one reduces ad revenue. Furthermore, large companies that own app stores benefit from more apps, translating into more ads and higher profits.

But Are Super Apps Really Inconvenient?

Yes, super apps often resemble “a miniature internet within an app,” leading to bloated and complex user interfaces. They can experience stability issues due to high demand and excessive load, and the attempt to merge dozens of services often results in primary and secondary functions, with the latter receiving fewer resources and less popularity.

A popular “Blue” social network from the US had to create a separate messaging app and restrict communication features in the main app due to super app pressures on the social network’s infrastructure. A major global search engine even reduced resource allocation for new features in its navigation service because of limited resources, especially during the chip shortage.

In Russia, attempts to actively implement super apps led to user dissatisfaction. A major bank and a large IT company began “unpacking” their super apps into separate applications, allowing them to focus on providing a great user experience.

What’s Next?

I believe super apps will eventually reach Western countries, driven by demographic trends.

According to Gartner research, young Americans are more interested in mobile games, new social networks, and other digital services that align with super app frameworks. They’re also more trusting of large tech companies and less concerned about sharing their data with these platforms.

As these generations grow in numbers and purchasing power, they’ll likely drive demand for super apps. Even “older” generations are catching up. A 2022 Pew Research Center study found that Americans over 64 are increasingly interested in new digital technologies and more likely to own smartphones than ever before. The report also noted that social media use among older Americans has quadrupled since 2010.

This trend is hard to stop. I believe similar patterns can be observed in Europe and Russia as well. The number of smartphones is increasing, and people are becoming more active users.

Moreover, people are getting lazier when it comes to managing a plethora of apps on their smartphones. Think about what’s easier: buying an airline ticket through a banking app with quick autofill and instant payment, or downloading the airline’s app, signing in, and navigating a different UX/UI to make a purchase?

Does this mean we’ll have our own versions of China’s “Yellow” super app? I think it’s important to look beyond that. The Chinese super app emerged in response to a need for digital services on smartphones without banks. Companies trying to copy China’s super apps will likely fail. Our world, where many people have desktop computers and experience with online services, will have a different demand for super apps.

What will they look like? We’ll soon see. But I’m sure they won’t succeed without AI. Imagine buying a ticket in a super app without an interface—just voice commands like, “Tickets from Istanbul to Phuket, leaving tomorrow, window seat, plus baggage,” and the app completes the transaction. This future is not far off.